》Check SMM Copper Quotes, Data, and Market Analysis

》Click to View SMM Spot Copper Historical Price Trends

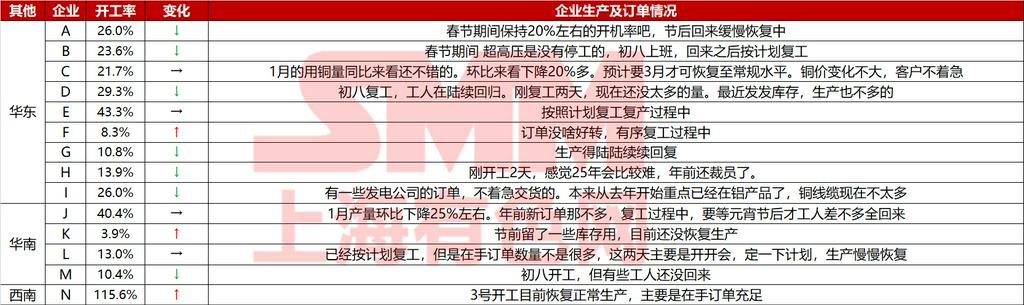

This week (1.31-2.6), the operating rate of SMM wire and cable enterprises was 27.36%, down by 15.48 percentage points compared to the last week before the Chinese New Year and 23.3 percentage points lower than the first week after the Chinese New Year in 2024 (due to differences in the number of working days). According to SMM, most enterprises in the industry resumed work as planned on the eighth day of the Chinese New Year, while a few extended their holiday until the tenth day. Since there were only two working days this week, the operating rate of wire and cable enterprises remained at a low level. During the holiday, some enterprises with ultra-high voltage orders continued production without interruption. Currently, new orders in the market have not yet materialized, and end-user enterprises are also gradually resuming work. Enterprises generally expect that new orders may not emerge until after the Lantern Festival. Additionally, the post-holiday rise in copper prices has dampened downstream customers' procurement sentiment.

Data Source: SMM

This week, the raw material inventory of wire and cable enterprises recorded 19,510 mt, down by 6.74% compared to pre-holiday levels and 23.73% lower than the first week after the Chinese New Year in 2024. This was partly due to differences in post-holiday working days and partly because enterprises indeed reduced their raw material procurement volume this year. Meanwhile, the finished product inventory of wire and cable enterprises recorded 18,310 mt this week, down by 5.62% compared to pre-holiday levels, mainly because enterprises focused on consuming finished product inventories as production had not yet fully resumed. Compared to the same period in the lunar calendar last year, the finished product inventory remained almost unchanged.

As some workers are still returning to work before the Lantern Festival, SMM expects the operating rate of wire and cable enterprises to rebound by 21.52 percentage points to 48.88% next week (2.7-2.13), though still 16.41 percentage points lower than the same period in the lunar calendar last year (the second week after the Chinese New Year). Regarding orders on hand, some enterprises reported receiving a significant number of power generation-related orders before the Chinese New Year, sufficient to meet their near-term production needs. Although power grid orders were tendered by the end of 2024, actual placements may not occur until March. Overall, wire and cable enterprises are unlikely to return to normal levels in February and may need to wait until March.